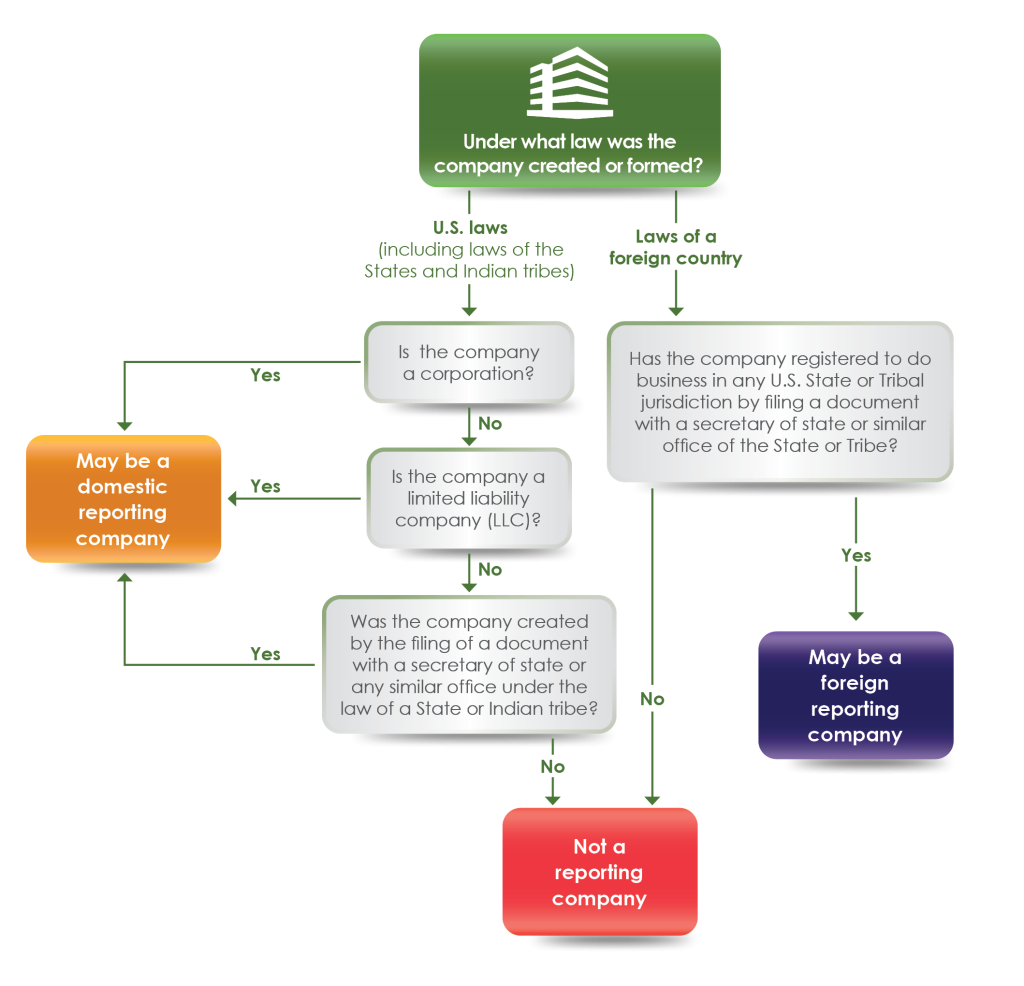

Companies required to report are called reporting companies. There are two types of reporting companies:

- Domestic reporting companies are corporations, limited liability companies, and any other entities created by the filing of a document with a secretary of state or any similar office in the United States.

- Foreign reporting companies are entities (including corporations and limited liability companies) formed under the law of a foreign country that have registered to do business in the United States by the filing of a document with a secretary of state or any similar office.

There are 23 types of entities that are exempt from the reporting requirements (see Question C.2). Carefully review the qualifying criteria before concluding that your company is exempt.

FinCEN’s Small Entity Compliance Guide for beneficial ownership information reporting includes the following flowchart to help identify if a company is a reporting company (see Chapter 1.1, “Is my company a “reporting company”?”).

[Issued September 18, 2023]

Yes, 23 types of entities are exempt from the beneficial ownership information reporting requirements. These entities include publicly traded companies meeting specified requirements, many nonprofits, and certain large operating companies.

The following table summarizes the 23 exemptions:

| Exemption No. | Exemption Short Title |

|---|---|

| 1 | Securities reporting issuer |

| 2 | Governmental authority |

| 3 | Bank |

| 4 | Credit union |

| 5 | Depository institution holding company |

| 6 | Money services business |

| 7 | Broker or dealer in securities |

| 8 | Securities exchange or clearing agency |

| 9 | Other Exchange Act registered entity |

| 10 | Investment company or investment adviser |

| 11 | Venture capital fund adviser |

| 12 | Insurance company |

| 13 | State-licensed insurance producer |

| 14 | Commodity Exchange Act registered entity |

| 15 | Accounting firm |

| 16 | Public utility |

| 17 | Financial market utility |

| 18 | Pooled investment vehicle |

| 19 | Tax-exempt entity |

| 20 | Entity assisting a tax-exempt entity |

| 21 | Large operating company |

| 22 | Subsidiary of certain exempt entities |

| 23 | Inactive entity |

FinCEN’s Small Entity Compliance Guide includes this table and checklists for each of the 23 exemptions that may help determine whether a company meets an exemption (see Chapter 1.2, “Is my company exempt from the reporting requirements?”). Companies should carefully review the qualifying criteria before concluding that they are exempt. Please see additional FAQs about reporting company exemptions in “L. Reporting Company Exemptions” below.

[Issued September 18, 2023]It depends. A domestic entity such as a statutory trust, business trust, or foundation is a reporting company only if it was created by the filing of a document with a secretary of state or similar office. Likewise, a foreign entity is a reporting company only if it filed a document with a secretary of state or a similar office to register to do business in the United States.

State laws vary on whether certain entity types, such as trusts, require the filing of a document with the secretary of state or similar office to be created or registered.

- If a trust is created in a U.S. jurisdiction that requires such filing, then it is a reporting company, unless an exemption applies.

Similarly, not all states require foreign entities to register by filing a document with a secretary of state or a similar office to do business in the state.

- However, if a foreign entity has to file a document with a secretary of state or a similar office to register to do business in a state, and does so, it is a reporting company, unless an exemption applies.

Entities should also consider if any exemptions to the reporting requirements apply to them. For example, a foundation may not be required to report beneficial ownership information to FinCEN if the foundation qualifies for the tax-exempt entity exemption.

Chapter 1 of FinCEN’s Small Entity Compliance Guide (“Does my company have to report its beneficial owners?”) may assist companies in identifying whether they need to report.

[Issued November 16, 2023]No. The registration of a trust with a court of law merely to establish the court’s jurisdiction over any disputes involving the trust does not make the trust a reporting company.

[Issued November 16, 2023]Sometimes. A reporting company is (1) any corporation, limited liability company, or other similar entity that was created in the United States by the filing of a document with a secretary of state or similar office (in which case it is a domestic reporting company), or any legal entity that has been registered to do business in the United States by the filing of a document with a secretary of state or similar office (in which case it is a foreign reporting company), that (2) does not qualify for any of the exemptions provided under the Corporate Transparency Act. An entity’s activities and revenue, along with other factors in some cases, can qualify it for one of those exemptions. For example, there is an exemption for certain inactive entities, and another for any company that reported more than $5 million in gross receipts or sales in the previous year and satisfies other exemption criteria. Neither engaging solely in passive activities like holding rental properties, for example, nor being unprofitable necessarily exempts an entity from the BOI reporting requirements.

FinCEN’s Small Entity Compliance Guide provides additional information concerning exemptions in Chapter 1.2, “Is my company exempt from the reporting requirements?”

[Issued December 12, 2023]No, unless a sole proprietorship was created (or, if a foreign sole proprietorship, registered to do business) in the United States by filing a document with a secretary of state or similar office. An entity is a reporting company only if it was created (or, if a foreign company, registered to do business) in the United States by filing such a document. Filing a document with a government agency to obtain (1) an IRS employer identification number, (2) a fictitious business name, or (3) a professional or occupational license does not create a new entity, and therefore does not make a sole proprietorship filing such a document a reporting company.

[Issued December 12, 2023]A beneficial owner is an individual who either directly or indirectly: (1) exercises substantial control (see Question D.2) over the reporting company, or (2) owns or controls at least 25% of the reporting company’s ownership interests (see Question D.4).

FinCEN’s Small Entity Compliance Guide provides checklists and examples that may assist in identifying beneficial owners (see Chapter 2.3 “What steps can I take to identify my company’s beneficial owners?”).

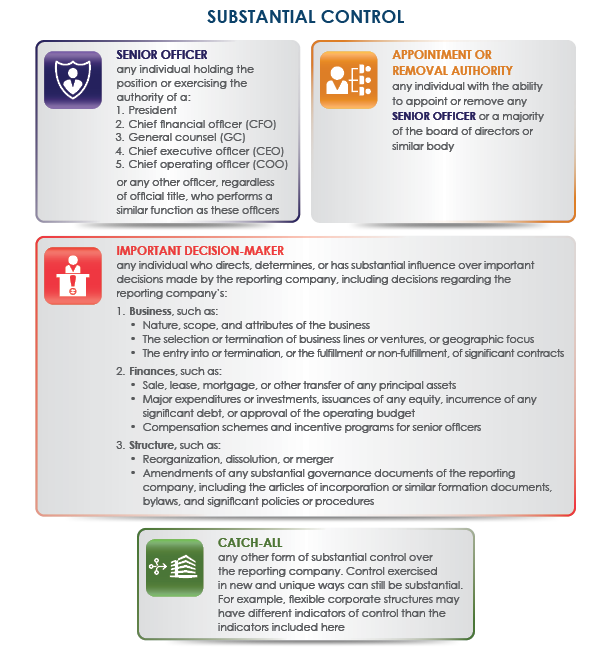

[Issued September 18, 2023]An individual can exercise substantial control over a reporting company in four different ways. If the individual falls into any of the categories below, the individual is exercising substantial control:

- The individual is a senior officer (the company’s president, chief financial officer, general counsel, chief executive office, chief operating officer, or any other officer who performs a similar function).

- The individual has authority to appoint or remove certain officers or a majority of directors (or similar body) of the reporting company.

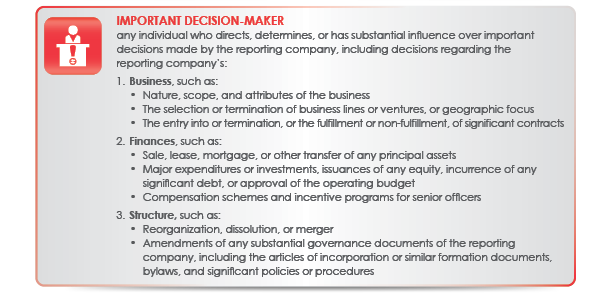

- The individual is an important decision-maker for the reporting company. See Question D.3 for more information.

- The individual has any other form of substantial control over the reporting company as explained further in FinCEN’s Small Entity Compliance Guide (see Chapter 2.1, “What is substantial control?”).

Important decisions include decisions about a reporting company’s business, finances, and structure. An individual that directs, determines, or has substantial influence over these important decisions exercises substantial control over a reporting company. Chapter 2.1, “What is substantial control?” of FinCEN’s Small Entity Compliance Guide provides the following information:

An ownership interest is generally an arrangement that establishes ownership rights in the reporting company. Examples of ownership interests include shares of equity, stock, voting rights, or any other mechanism used to establish ownership.

Chapter 2.2, “What is ownership interest?” of FinCEN’s Small Entity Compliance Guide discusses ownership interests and sets out steps to assist in determining the percentage of ownership interests held by an individual.

[Issued September 18, 2023]There are five instances in which an individual who would otherwise be a beneficial owner of a reporting company qualifies for an exception. In those cases, the reporting company does not have to report that individual as a beneficial owner to FinCEN.

FinCEN’s Small Entity Compliance Guide includes a checklist to help determine whether any exceptions apply to individuals who might otherwise qualify as beneficial owners (see Chapter 2.4. “Who qualifies for an exception from the beneficial owner definition?”).

[Issued September 18, 2023]Accountants and lawyers generally do not qualify as beneficial owners, but that may depend on the work being performed.

Accountants and lawyers who provide general accounting or legal services are not considered beneficial owners because ordinary, arms-length advisory or other third-party professional services to a reporting company are not considered to be “substantial control” (see Question D.2). In addition, a lawyer or accountant who is designated as an agent of the reporting company may qualify for the “nominee, intermediary, custodian, or agent” exception from the beneficial owner definition.

However, an individual who holds the position of general counsel in a reporting company is a “senior officer” of that company and is therefore a beneficial owner. FinCEN’s Small Entity Compliance Guide includes a checklist to help determine whether an individual qualifies for an exception to the beneficial owner definition (see Chapter 2.4, “Who qualifies for an exception from the beneficial owner definition?”).

[Updated November 16, 2023]If a beneficial owner owns or controls their ownership interests in a reporting company exclusively through multiple exempt entities, then the names of all of those exempt entities may be reported to FinCEN instead of the individual beneficial owner’s information.

- Note that this special rule does not apply when an individual owns or controls ownership interests in a reporting company through both exempt and non-exempt entities. In that case, the reporting company must report the individual as a beneficial owner (if no exception applies), but the exempt companies do not need to be listed.

FinCEN’s Small Entity Compliance Guide includes more information about this special reporting rule in Chapter 4.2, “What do I report if a special reporting rule applies to my company?”

[Issued September 29, 2023]The unaffiliated company itself cannot be a beneficial owner of the reporting company because a beneficial owner must be an individual. Any individuals that exercise substantial control over the reporting company through the unaffiliated company must be reported as beneficial owners of the reporting company. However, individuals who do not direct, determine, or have substantial influence over important decisions made by the reporting company, and do not otherwise exercise substantial control, may not be beneficial owners of the reporting company.

Please see Chapter 2.1 of FinCEN’s Small Entity Compliance Guide, “What is substantial control?” for additional information on how to determine whether an individual has substantial control over a reporting company.

[Issued September 29, 2023]No. A beneficial owner of a company is any individual who, directly or indirectly, exercises substantial control over a reporting company, or who owns or controls at least 25 percent of the ownership interests of a reporting company.

Whether a particular director meets any of these criteria is a question that the reporting company must consider on a director-by-director basis.

FinCEN’s Small Entity Compliance Guide includes additional information on how to determine if an individual qualifies as a beneficial owner in Chapter 2, “Who is a beneficial owner of my company?”. This chapter includes separate sections with more information about substantial control and ownership interest: Chapter 2.1 “What is substantial control?” and Chapter 2.2 “What is ownership interest?”

[Issued September 29, 2023]It depends. A reporting company’s “partnership representative,” as defined in 26 U.S.C. 6223, or “tax matters partner,” as the term was previously defined in now-repealed 26 U.S.C. 6231(a)(7), is not automatically a beneficial owner of the reporting company. However, such an individual may qualify as a beneficial owner of the reporting company if the individual exercises substantial control over the reporting company, or owns or controls at least 25 percent of the company’s ownership interests.

Chapter 2 of FinCEN’s Small Entity Compliance Guide (“Who is a beneficial owner of my company?”) has additional information on how to determine if an individual qualifies as a beneficial owner of a reporting company.

Note that a “partnership representative” or “tax matters partner” serving in the role of a designated agent of the reporting company may qualify for the “nominee, intermediary, custodian, or agent” exception from the beneficial owner definition.

FinCEN’s Small Entity Compliance Guide includes additional information on such exemptions in Chapter 2.4, “Who qualifies for an exception from the beneficial owner definition?”

[Issued November 16, 2023]